QROPS in Australia

In Australia, pension income from a QROPS is subject to the individual’s marginal income tax rate, which varies between 0% and 45%, depending on total assessable income.

Who This Is For

Who This Is Not For

Managing international pensions for UK expats requires a strategic approach to maximizing benefits, reducing tax liabilities and securing long-term financial stability. Many UK nationals moving abroad fail to optimize their pensions, leading to unnecessary tax burdens and missed investment opportunities. Without a proper expat pension plan, individuals risk losing access to tax-efficient retirement schemes, facing currency fluctuations and paying more in overseas pension taxation.

Understanding how much to save for retirement is a key consideration for UK expats. The right pension plan should align with your financial goals, offer flexibility in withdrawals and ensure compliance with local pension laws in your chosen new country of residence.

To make informed decisions about your retirement planning, consider our pension advisory service, which helps you navigate the complex world of international pension schemes. Our pension advisors specialize in offering tailored advice for tax-efficient pension transfers and strategic financial planning, ensuring your retirement savings are optimized for both local and international regulations. With expert guidance from our pension advisory service, you can confidently plan for a secure retirement abroad. A financial advisor for pensions can help you navigate the complexities of UK pension transfers, ensuring you make tax-efficient decisions that maximize your retirement savings.

Different countries impose varying tax rates on pension withdrawals and not all UK pension schemes are tax-efficient for expats. Many UK retirees choose to establish pensions in Malta, pensions in Gibraltar or pensions in Portugal because these jurisdictions offer favourable tax treatment under Double Taxation Agreements (DTAs). Understanding how DTAs work can help you avoid paying UK tax on overseas pensions and reduce pension transfer costs.

To understand how tax can impact your pension abroad, explore tax planning for UK expats for expert advice.

HMRC explains residency rules in the UK statutory residence test guidance.

Moreover, UK expats need to protect their pension assets from inflation, currency fluctuations and regulatory risks. This is where international pension schemes such as:

International Pension Plans come into play, providing flexible, tax-efficient retirement solutions tailored for UK expatriates.

Book Your Free 15-Minute Exit Strategy Call.

Limited private strategy slots available each week.

Trusted by UK nationals globally.

Prefer to speak directly? Tel: +44 208 058 8937.

Email: connect@adviceforexpats.com.

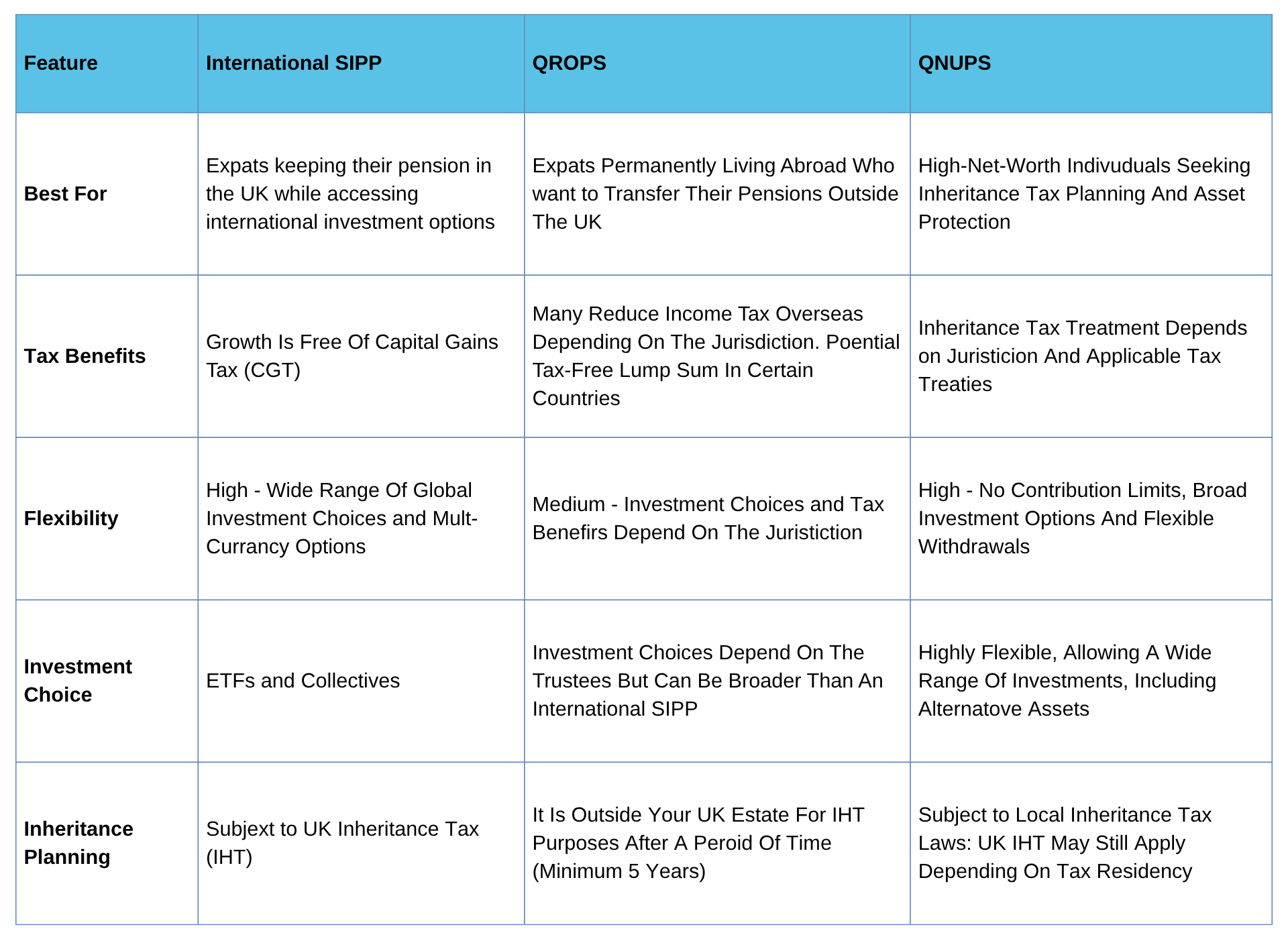

While International SIPPs are an ideal solution for many UK expats, international pension plans provide another flexible, tax-efficient solution for individuals who require a global retirement option that works across multiple countries and financial systems.

One of the biggest advantages of an International SIPP is that it enables tax-efficient retirement planning, allowing UK expats to diversify their pension investments, access global markets and choose a multi-currency structure. This makes SIPP pensions an excellent option for UK nationals living in Europe, the Middle East, Asia or beyond.

For wider support alongside pensions, explore financial services for UK expats for expert guidance.

Many UK expats choose International SIPPs because they remain under UK regulatory protection while offering greater international flexibility than traditional workplace pensions.

An International SIPP can help UK expats consolidate pension arrangements, manage investments across multiple currencies and structure retirement income more efficiently alongside international tax residency planning.

Unlike many domestic UK pension arrangements, International SIPPs are specifically designed to accommodate internationally mobile lifestyles and cross-border retirement planning needs.

For UK expats living overseas long term, pension flexibility alone is not enough — pension income withdrawals, tax residency, reporting obligations and succession planning must also be coordinated carefully.

Professional pension advice is essential because poorly structured pension decisions can trigger unnecessary tax exposure, transfer charges or inefficient retirement income planning later.

Many UK expats accumulate multiple UK pension schemes over time, often resulting in fragmented investment strategies, duplicated fees and poor long-term visibility over retirement income planning.

An International SIPP can simplify pension management by consolidating eligible pensions into a single structure with improved oversight, broader investment flexibility and easier long-term retirement planning.

For many UK expats, International SIPPs provide a practical alternative to QROPS because they remain UK regulated while still accommodating international retirement planning requirements.

Consolidation may also improve cost efficiency, investment coordination and retirement income planning, particularly where older pension arrangements contain inconsistent charging structures or outdated investment options.

Before consolidating pensions, UK expats should assess tax residency, pension type, transfer restrictions, safeguarded benefits and long-term withdrawal strategy to avoid unintended tax or regulatory consequences.

One of the key advantages of an International SIPP is that assets grow tax-free until withdrawals are made, allowing pension savings to compound efficiently over time. Taxes only apply upon withdrawal, and the tax treatment depends on your country of tax residency. If a Double Taxation Agreement (DTA) is in place, it may provide reduced tax rates or exemptions, making pension withdrawals more tax-efficient for UK expats.

To model sustainable withdrawals, use the pension drawdown calculator to estimate annual income.

For UK expats living abroad, currency fluctuations can significantly impact retirement income, making multi-currency flexibility a crucial feature of an International SIPP. This type of pension allows expats to hold and invest in multiple currencies, including GBP, EUR, USD and other major global currencies, reducing exchange rate risks and ensuring that pension withdrawals align with their country of residence.

By keeping pension assets in a currency that matches future expenses, UK expats can protect their retirement savings from currency volatility and have greater control over their withdrawal strategy to meet financial needs. British nationals can also withdraw funds in their preferred currency, minimizing conversion costs and ensuring financial stability in retirement.

Unlike standard UK workplace pensions, an International SIPP provides UK expats with access to a diverse selection of funds in multiple currencies, offering greater flexibility compared to domestic SIPPs, which are primarily GBP-denominated and UK-focused. Unlike domestic SIPPs, which are designed for UK residents, International SIPPs provide access to funds tailored for non-UK residents, offering more relevant investment opportunities that align with global markets and expat financial needs.

An International SIPP remains under the regulation of the UK Financial Conduct Authority (FCA), ensuring a high level of security and investor protection that offshore pension schemes, such as QROPS, may not offer. FCA oversight guarantees strict compliance with UK pension regulations, providing greater transparency and accountability compared to some offshore pension plans. This makes an International SIPP an ideal option for UK expats who wish to maintain a UK-based pension arrangement while benefiting from robust financial safeguards. For expats who require a UK-compliant pension structure, an International SIPP ensures regulatory protection while providing the flexibility of international investment options.

An International SIPP offers flexible withdrawal options, allowing UK expats to align their pension income with other retirement earnings for better financial planning. Lump sums or phased withdrawals can be accessed based on individual needs, with the option to delay withdrawals in high-tax years to reduce tax exposure.

Coordinating withdrawals with other income streams ensures tax efficiency and helps optimize retirement cash flow. This level of income planning flexibility enables UK expats to structure their finances strategically, ensuring their retirement savings are managed effectively.

For UK expats who may eventually return to the UK, an International SIPP provides greater flexibility compared to QROPS. If an expat moves back to the UK, their pension remains within UK jurisdiction without requiring complex transfers, simplifying the transition and ensuring continued access to retirement funds.

Unlike some offshore pension schemes, an International SIPP remains fully compliant within the UK, ensuring a smooth transition if you decide to return home. Additionally, an International SIPP imposes no restrictions on relocating between countries, making it a suitable option for those living in Europe, the Middle East Asia, or beyond.

Important Note: While an International SIPP offers many advantages, it is still subject to UK pension rules and withdrawals are taxable under UK law unless tax residency in another jurisdiction provides exemptions via a Double Taxation Agreement (DTA).

Choosing the best pension option is essential. Our pension advisors can help you determine whether an International SIPP, QROPS or QNUPS is best for your retirement needs.

In addition to QROPS, QNUPS, and International SIPPs, International Pension Plans offer an attractive alternative for expats seeking global retirement solutions. They allow for better flexibility across various jurisdictions, especially for those moving between countries.

If you are keeping your pension in the UK, an International SIPP is often the best choice.

If you are permanently moving overseas, QROPS might provide greater tax advantages, however the Overseas Transfer Allowance (OTA) formerly referred to as the Lifetime Allowance Charge (LTC), and the Overseas Transfer Charge (OTC) make render a transfer uneconomic.

While most expats opt for defined contribution pensions, some may still qualify for a defined benefit pension based on their previous UK employment. A defined benefit pension can offer guaranteed income in retirement, which may be appealing for those looking for financial security in their later years.

You can estimate transfer value using a CETV transfer value calculator to compare options.

For inheritance tax planning, QNUPS used to be the best option but following the UK Autumn Budget it offers no protection for UK Inheritance Tax purposes. An international pension plan is a better choice.

Want expert guidance? Our panel of experienced pension specialists can help you navigate the complexities of International SIPPs, QROPS, QNUPS or international pension plans such as Guernsey’s Section (40) ee pension schemes; ensuring you choose the most tax-efficient and flexible pension option based on your financial goals and country of residence.

A Qualifying Recognised Overseas Pension Scheme (QROPS) is an HMRC-recognized pension that allows UK expats to transfer their UK pension to an overseas scheme. QROPS are designed to provide greater tax efficiency, investment flexibility and estate planning benefits for those permanently living outside the UK.

UK expats often consider transferring to a QROPS to reduce tax liabilities, protect pension assets from UK legislation changes and secure inheritance tax planning advantages. However, QROPS are not suitable for everyone, and suitability depends on country of tax residency and retirement goals.

Speak with our expert pension advisors to determine whether a QROPS transfer aligns with your retirement strategy and tax planning needs.

For detailed information on transferring your UK pension, refer to The pensions regulator’s dealing with transfer requests page.

A Defined Benefit (DB) pension is a retirement plan where the amount you receive in retirement is determined by factors such as your salary and years of service. This type of pension offers guaranteed income, making it an attractive option for many employees.

DB pensions provide security, as they promise a set income in retirement. However, they are becoming increasingly rare, with many employers switching to defined contribution (DC) schemes. Pension advisors, supported by a qualified pensions actuary, can help you understand how it works and whether it aligns with your retirement objectives.

A QROPS allows pension assets to grow free from local capital gains tax (CGT) while inside the pension scheme. However, tax on withdrawals varies depending on the UK expat’s country of residence and the specific tax rules in place. Some jurisdictions offer lower or zero tax rates (in Dubai), while others may apply standard income tax rates to pension withdrawals. Additionally, UK tax rules may still apply if the individual remains UK tax resident or returns to the UK within a specific timeframe. Proper tax planning and pension advice are essential to optimize withdrawals under local tax laws and Double Taxation Agreements (DTAs) where applicable.

FCA transfer standards are set out in COBS 19.1 pension transfer rules.

QROPS allow expats to hold pension funds in multiple currencies reducing foreign exchange risks and aligning pension withdrawals with their country of residence.

After five years of non-UK residency, a QROPS is typically outside of the UK estate for UK inheritance tax purposes, potentially offering significant wealth preservation benefits.

A QROPS is only a viable option when both the pension scheme and the individual member reside in the same country. If a UK national moves to Malta, Gibraltar, Ireland, New Zealand or Australia and transfers their pension into an HMRC listed ROPS scheme in that country, they are not subject to the UK Overseas Transfer Charge (OTC). Each jurisdiction has different tax rates on pension income and regulatory frameworks, which should be carefully considered when deciding where to transfer a UK pension.

QROPS in Australia

QROPS in New Zealand

QROPS in Ireland

QROPS in Malta

QROPS in Gibraltar

QROPS jurisdictions vary in tax treatment and regulations, making it essential to choose a location that aligns with your retirement and tax planning needs.

Transferring your UK pension to a QROPS requires careful planning to ensure tax efficiency and compliance with both UK and local tax regulations.

HMRC pension transfer guidance to remain tax-efficient and compliant.

Be aware that delays in UK pension transfers can occur, especially if paperwork is incomplete or compliance checks by UK pension providers take longer than expected due to the requirements of the Pension Schemes Act 2021.

Our specialists proactively handle the entire transfer process to reduce these delays, ensuring your pension funds are transferred smoothly and efficiently.

Be aware of potential pension transfer delays when moving your UK pension abroad. These delays can impact your retirement timeline, so it’s important to plan ahead and ensure the paperwork and transfers are managed efficiently.

If QROPS isn’t the right choice for you, an International Pension Plan could offer a more suitable global retirement solution, particularly for individuals seeking broader options than traditional pension schemes. These plans are especially beneficial for those who need flexibility across various countries.

Independent guidance is available on the MoneyHelper pension transfer page.

A Qualifying Non-UK Pension Scheme (QNUPS) is typically used by affluent UK expats and high-net-worth individuals seeking long-term wealth accumulation, investment flexibility and international pension structuring opportunities.

Unlike traditional UK pension structures, QNUPS do not operate under standard UK contribution limits, making them attractive for individuals who have already maximised UK pension allowances.

Historically, QNUPS were widely used for inheritance tax planning. However, following the UK’s shift toward residency-based inheritance tax treatment, their historic estate-planning advantages have been materially reduced.

Despite this change, QNUPS continue to offer several benefits, including unrestricted investment flexibility, multi-currency options and no lifetime contribution limits.

Despite these changes, QNUPS can still offer investment flexibility, multi-currency structuring and long-term wealth accumulation opportunities for certain UK nternationally mobile families.

However, QNUPS should no longer be viewed as a simple inheritance tax solution and must now be assessed within the context of wider cross-border estate planning and residency strategy.

For wider estate planning considerations, review our estate planning for UK expats guide covering inheritance tax exposure, succession planning and international asset structuring.

Unlike UK pension schemes, QNUPS have no limits on contributions or investment options, making them a versatile tool for wealth management.

QNUPS are not restricted by UK pension contribution caps, allowing high-net-worth individuals to accumulate pension wealth efficiently.

Expats can invest in a wide range of asset classes and hold their pension in multiple currencies to mitigate foreign exchange risks.

While no longer an automatic UK IHT shield, QNUPS may still provide estate planning advantages, depending on jurisdictional tax laws.

International Pension Plans (IPPs) are internationally portable retirement structures designed for globally mobile professionals, entrepreneurs and high-net-worth individuals seeking long-term retirement flexibility across multiple jurisdictions.

Unlike many traditional UK pension arrangements, International Pension Plans are often designed for individuals who expect to live, work or retire across multiple countries during their lifetime.

These plans can provide broader international investment access, multi-currency flexibility and greater portability for internationally mobile UK expats.

Depending on the jurisdiction and provider, some International Pension Plans may offer fewer UK-specific restrictions, wider investment flexibility and more internationally focused retirement planning opportunities.

Jurisdiction selection should never be based solely on tax treatment. Regulatory quality, treaty interaction, reporting obligations, succession planning and long-term residency strategy must also be considered carefully.

Book My Free 15-Minute Exit Strategy Call.

Limited private strategy slots available each week.

Trusted by UK nationals globally.

Prefer to speak directly? Tel: +44 208 058 8937.

Email: connect@adviceforexpats.com.

The tax treatment of overseas pensions depends on the country in which you have established fiscal residency.

The Overseas Transfer Charge (OTC) is a 25% tax applied to UK pension transfers to a QROPS, if the scheme, is located in a country, where the individual is not a tax resident at the time of transfer.

However, transfers to HMRC-approved ROPS schemes in Malta, Gibraltar, Ireland, New Zealand, Australia and other qualifying jurisdictions are exempt from the OTC if the individual is a tax resident in the same country as the QROPS pension trustees. Official rules are published in the overseas transfer charge guidance.

Planning how your pension is passed on is essential for UK expats. The tax treatment of pensions upon death depends on the type of pension scheme, your residency and the age at which you pass away. Understanding these factors ensures your beneficiaries receive the maximum possible benefit.

In addition to private pensions, it’s crucial to include a pension forecast for your UK state pension to better understand the total retirement income you can expect, especially if you are receiving a UK state pension while living abroad.

Retirement planning for UK expats should not focus purely on pension size. Long-term retirement security also depends on tax residency, healthcare costs, inflation exposure, currency risk and how pension withdrawals are structured internationally.

The amount required for retirement varies significantly depending on country of residence, lifestyle expectations, healthcare access, property ownership and taxation of pension income locally.

Many UK expats underestimate the long-term impact of inflation, exchange-rate volatility and international taxation on retirement income sustainability.

Retirement planning should therefore coordinate pension strategy, withdrawal sequencing, tax efficiency and long-term estate planning rather than focusing purely on headline pension values.

The amount needed for a comfortable retirement abroad varies based on lifestyle, location, and personal financial goals. Some countries offer a lower cost of living, while others require a larger pension fund to maintain financial security. Below are some general guidelines for UK expats in estimating their retirement savings.

Some destinations offer significantly lower living costs than the UK, while others require a larger pension fund.

Pension scams targeting UK expats have become increasingly sophisticated, with fraudsters exploiting gaps in regulation, offshore investment schemes and misinformation about pension transfers. Expats seeking tax efficiency and higher returns on their retirement funds can often become prime targets for unscrupulous operators. Losing your pension to a scam can have devastating financial consequences, making it crucial to stay informed and vigilant.

FCA ScamSmart explains how to spot and avoid pension scams.

Fraudulent pension schemes can wipe out your retirement savings, making it crucial to take proactive steps to safeguard your funds. Staying informed and working with regulated professionals can help you avoid costly mistakes.

Navigating pension transfers, tax liabilities and international regulations as a UK expat can be complex. Without the right advice, you could face unexpected tax bills, compliance issues or financial losses. Seeking expert guidance ensures your pension is tax-efficient, secure and aligned with your long-term retirement goals. Official retirement rules are explained in UK government retiring abroad guidance.

Avoid Unnecessary Tax Liabilities: Transferring or withdrawing your pension incorrectly can trigger hefty tax charges. A regulated pension adviser can provide tax-efficient solutions.

Ensure Your Pension is Secure & Compliant: Some offshore pension schemes lack proper regulation. An FCA-regulated adviser helps you avoid scams and high-risk investments.

Get a Personalized Retirement Plan: Every UK expat has unique financial needs. The right pension structure depends on your country of residence, tax status and long-term retirement goals.

Protect your wealth before executing irreversible financial decisions.

Tel: +44 208 058 8937 or Email: connect@adviceforexpats.com.

At Advice for Expats, we offer expert international pension advice and retirement planning tailored to the unique needs of British expatriates. Whether you are considering an International SIPP, QROPS or QNUPS, our specialist advisers help you navigate the complexities of pension transfers, consolidation and tax-efficient retirement planning.

Our FCA-regulated network of pension specialists delivers clear, tailored strategies to ensure your retirement savings are optimised and protected—wherever you live.

We help British expats maximise pension benefits, avoid costly mistakes and choose the right pension structure for their residency, goals, and lifestyle. Trust us to align your pension plans with your aspirations, so your retirement is as rewarding as the life you have built across borders.

There is no single “best” pension for UK expats. The right option depends on your country of tax residence, pension type and long-term plans. Most UK expats consider International SIPPs, QROPS or international pension plans based on tax efficiency, flexibility and compliance.

Yes, usually. UK pensions are taxable based on your country of tax residence and the relevant Double Taxation Agreement. Some countries tax pension income at reduced rates, while others apply standard income tax rules.

It depends on your fiscal residency and long-term plans. An International SIPP keeps your pension under UK regulation. A QROPS may offer tax advantages if you are permanently resident overseas and meet local eligibility rules. Transfers must be assessed carefully to avoid the 25% Overseas Transfer Charge.

The amount UK expats need for retirement depends on taxation, healthcare costs, property ownership, exchange-rate exposure and lifestyle expectations in their chosen country. Lower-cost countries may require £300,000–£500,000 for modest retirement, while higher-cost jurisdictions often require significantly larger pension assets and tax-efficient withdrawal planning.

Use an FCA-regulated adviser, verify pension providers with official registers and avoid unsolicited transfer offers. Never rush decisions and always request full documentation before transferring funds.

The Overseas Transfer Charge is a 25% UK tax applied when transferring a pension to a QROPS in a country where you are not tax resident. It does not apply if the QROPS and your tax residence match approved conditions.

You can usually keep your UK pension where it is and draw it overseas. However, taxation depends on your country of residence and the applicable Double Taxation Agreement. Transfers are optional, not mandatory.

Yes. Many UK expats consolidate pensions into an International SIPP or suitable scheme to simplify management, reduce fees and improve investment control. Suitability must be assessed first.

QNUPS no longer provide automatic UK inheritance tax protection following recent UK changes. However, they may still offer long-term investment flexibility for high-net-worth individuals depending on structure and jurisdiction.

Usually yes. UK state pensions are generally taxable, but whether tax is paid in the UK or your country of residence depends on the relevant Double Taxation Agreement and your tax residency position abroad.

Yes. UK pensions can usually be accessed while living abroad, but taxation depends on your country of residence, pension type and the relevant Double Taxation Agreement. Poorly timed withdrawals can create unnecessary tax exposure if residency and treaty rules are not coordinated correctly.

Your pension remains valid and accessible. You may keep it in the UK or transfer it. The key issue is taxation and regulatory compliance, not access.

The best option depends on your tax residency, retirement location, pension value and long-term succession planning goals. Overseas pension transfers may offer advantages in some cases, but unnecessary transfers can trigger UK tax charges, compliance complications and avoidable long-term pension risk.

Usually yes. UK state pensions are generally taxable, but whether tax is paid in the UK or your country of residence depends on the relevant Double Taxation Agreement and your overseas tax residency position.

A QROPS (Qualifying Recognised Overseas Pension Scheme) is an HMRC-approved overseas pension that allows UK pensions to be transferred abroad, subject to eligibility and potential transfer charges.

The 25% tax refers to the Overseas Transfer Charge. It applies when a UK pension is transferred to a QROPS in a country where the member is not tax resident under HMRC rules.

Protect your pensions, investments and tax position before acting.

Tel: +44 208 058 8937 or Email: connect@adviceforexpats.com.